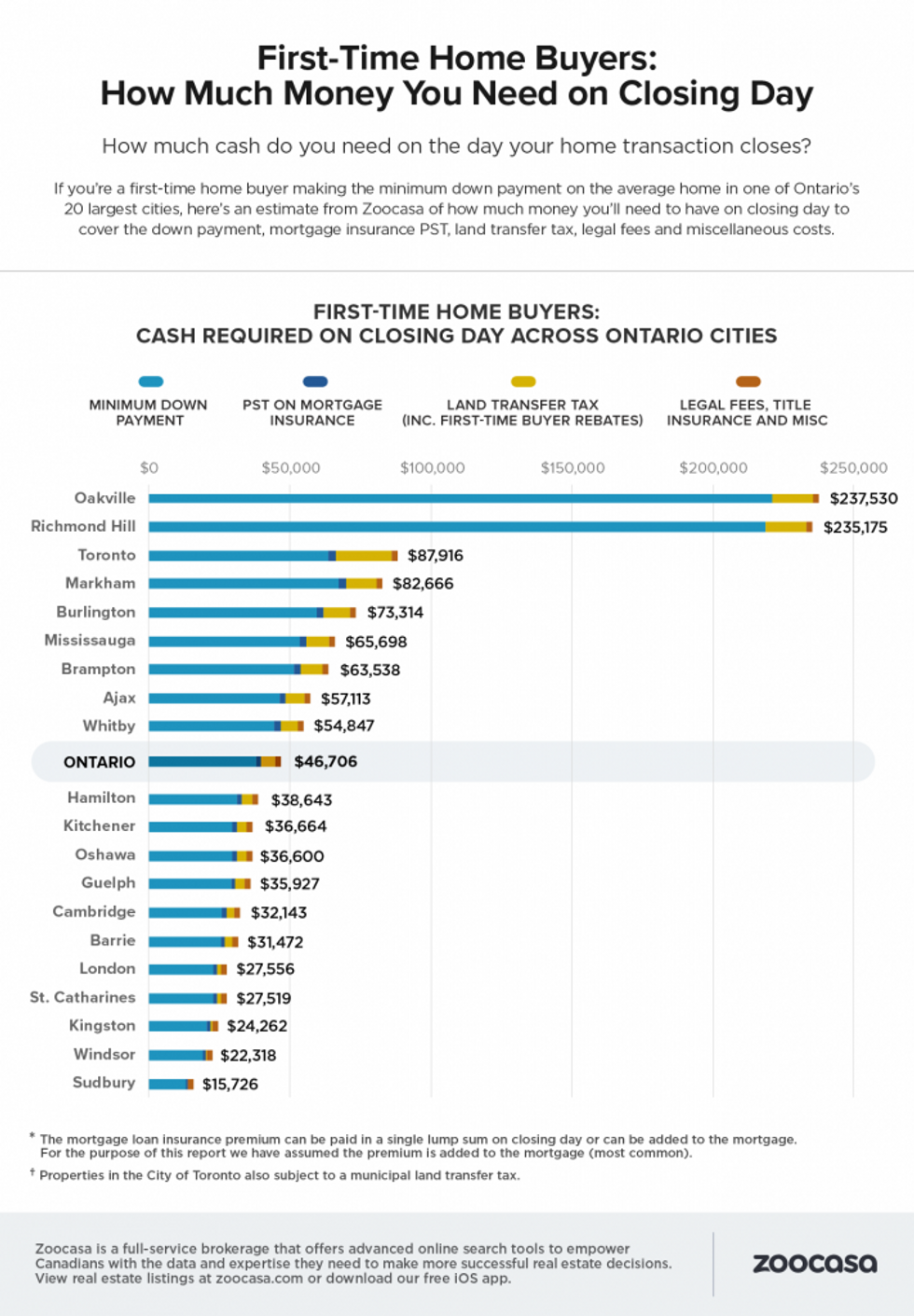

Table of Content

Finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service. You may also be able to find programs for forgivable grants, deferred payment second mortgages and fully amortizing second loans. Down payment assistance programs are often targeted toward certain groups, such as first-time homebuyers, active military members, veterans or teachers. Once the sale is official and the title is transferred from the previous owner to the new owner , taxes on the transaction are required to be paid as well. In some states the law requires that an attorney is present at the closing.

Some lenders, especially for government-backed loans, require you to have an inspection to ensure the home you’re buying doesn’t have any lead paint. The buyer is responsible for the cost, which can vary between $250 and $450. This fee is paid to the title company or escrow company that is conducting the closing. Their role is to oversee the transaction as a neutral third party. They also hold funds in an account during the transaction and disperse your down payment, fees and other charges to the appropriate individuals upon closing.

Survey fee

When you sell a home in Kentucky, you'll still have to pay property taxes for the months you owned the property. Using this prorated system, you won't be on the hook for the full 12 months of taxes. However, this does make it more difficult to estimate how much you'll owe at closing.

Check your buying power by getting pre-qualified for a mortgage with us at Zillow Home Loans. During a financed home purchase, several institutions need to process information and create official records. Paying close attention to both of these documents prepares you for the amount of cash you’ll need and when. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page.

Credit towards closing costs

This will list out every closing cost you need to cover and how much you owe. Let’s look at some of the most common closing costs you might see on your disclosure. Your down payment isn’t the only thing you need to bring to the closing table when you buy a home. Closing costs are expenses you pay to your lender in exchange for loan services. While the property tax rate can vary widely state to state, all 50 states have some form of property taxes. This one-time payment protects the future owner from the financial burden of sorting out title issues in court, whether they arise at closing or years down the road.

These include the costs of verifying and transferring ownership to the buyer, so most are unavoidable. Contact a few competing loan providers and ask what types of fees they charge. Choose a lender that offers low fees and competitive interest rates for lower overall closing costs.

Courier Fees

You'll also need to save an additional 3% – 6% of your loan value to cover closing costs, unless you can negotiate seller concessions or have some of the fees wrapped into your loan. Typically, the only closing costs that are tax deductible are payments toward mortgage interest – buying points – or property taxes. Both buyers and sellers pay closing costs, but as a seller, you can expect to pay more. Usually one of the largest line items at closing, an origination fee covers the lender’s administrative costs in opening your loan. It’s usually 1% of the total loan amount, but if you shop around, you may be able to find lower fees. If you finance your home with an FHA loan and pay less than 20% of the price of the home for your down payment, you’ll pay monthly a mortgage insurance premium .

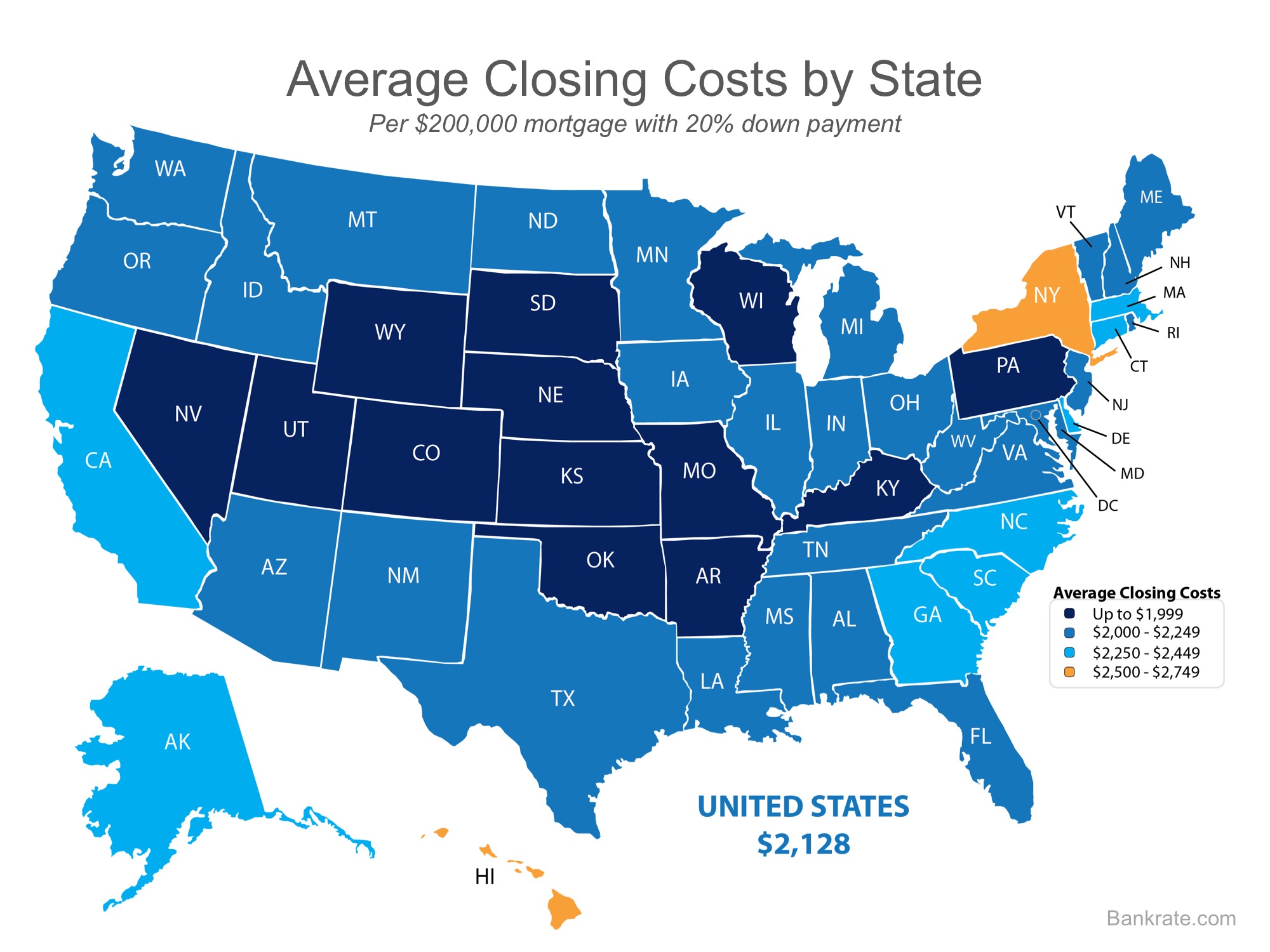

It’s important to understand your regional burden, as well as who usually pays closing costs in the transaction and when they’re due. Conventional loan closing costs range between 2% and 5% of the purchase price. If you make a down payment of less than 20%, you’ll pay private mortgage insurance until you reach a loan-to-value ratio of 78%, when you can request discontinuation of the payment. Buyer closing costs are a combination of one-time fees and the initial installments of recurring costs you’ll pay alongside your mortgage every month. An example of a recurring cost is your homeowners insurance premium.

Financial advisors recommend that your mortgage payment should be no more than 28% of your monthly household income. Considering that fact, here are the minimum required monthly incomes you need to afford this house based on your down payment. Here are the monthly payments for a $320,000 home loan based on a down payment and current mortgage rate averages from Freddie Mac as of December 15, 2022. To save on your home loan, consider comparing the fees and rates of top lenders before signing. Attorney fees — Depending on your state’s laws, you may not be required to have an attorney present at closing.

The government-mandated closing costs form is called a loan estimate . Typically the buyer pays closing costs, though sometimes negotiations between the buyer and the seller can lead to the seller paying some of the closing costs. Buyers and sellers in Louisiana pay an average of $325 in tax combined for the closing.

Across the state, the average home sells for between $200,000 and $300,000. If you buy a property in that range, expect to pay between $2,551.36 and $5,740.56 in closing costs after taxes. Every little fee adds up, so even if you can bring down the cost on only a few items, you could save yourself paying thousands of dollars in closing costs on your closing day. Lastly, you could also find out if you can defer your closing cost payments by rolling the closing costs into your mortgage.

We track the cost of each fee by city and state to give you the best estimate on closing costs. For example, they include the cost of the home appraisal and home title searches that lenders require. A more detailed list of closing costs appears below, and your real estate agent can help estimate yours for your area and loan type. Your lender will also tell you what you can expect to pay at closing after you apply for a mortgage, in a document called a Loan Estimate. At closing, buyers are often required to open an ongoing escrow account from which their mortgage servicer will pay ongoing costs. An escrow account is free to open or maintain because it’s a requirement for loans with less than 20% down.

Costs you can shop for amount to about $7,600, while fixed costs and fees are estimated to be $1,661. In some states, you’re actually required by state law to have a real estate attorney present when a home is bought or sold. If you do hire a lawyer, he or she will often be paid at closing, out of the proceeds from the sale. A transfer tax is a one-time tax or fee imposed by a state, county or local government whenever a property changes hands. It may be a flat fee or a percentage of the home price, and the cost can vary significantly by location.

Real estate commissions may vary, but the average rate is 5 – 6% of the purchase price. The buyer's agent and the seller's agent split the fee evenly. For buyers, it depends on your loan program, size of loan and individual lender practices. For sellers, it comes down to what you’ve negotiated in terms of concessions and agent commission.

Shop around for better prices

The general rule across the country is that home buyers pay the lion's share of closing costs. They can expect to fork over anywhere from 2-5% of the home's sale price, regardless of location. Kentucky closing costs are usually taken right out of your sale profits at closing.

Those service providers all have varying fees as well, so it can save you a lot on closing day to shop around upfront and carefully select the companies you choose to work with. To avoid an unpleasant surprise on closing day, it’s essential to know what happens at a house closing and the ins and outs of closing costs. Once you understand what you’re paying for, you’ll be in a much better position to negotiate the fees involved with a closing, before you sign the papers on closing day. Your total closing costs will ultimately vary based on your home's value, local fees, and negotiations with your buyer. While closing costs will always have to be paid, your real estate agent can often negotiate who pays them — you or the buyer. Seller closing costs are fees and taxes you pay when you finalize the sale of your home in Kentucky.

No comments:

Post a Comment